Page 416 - ES 2020-21_Volume-1-2 [28-01-21]

P. 416

State of the Economy 2020-21: A Macro View 43

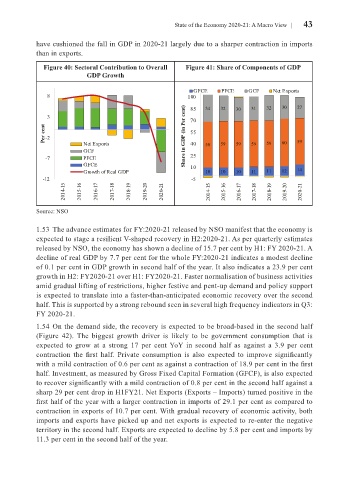

have cushioned the fall in GDP in 2020-21 largely due to a sharper contraction in imports

than in exports.

Figure 40: Sectoral Contribution to Overall Figure 41: Share of Components of GDP

GDP Growth

GFCE PFCE GCF Net Exports

8 100

3 85 34 32 30 31 32 30 27

70

Per cent -2 Share in GDP (in Per cent) 55 60 59

Net Exports

GCF 40 58 59 59 59 59

-7 PFCE 25

GFCE 10

Growth of Real GDP 10 10 10 11 11 12 14

-12 -5

2014-15 2015-16 2016-17 2017-18 2018-19 2019-20 2020-21 2014-15 2015-16 2016-17 2017-18 2018-19 2019-20 2020-21

Source: NSO

1.53 The advance estimates for FY:2020-21 released by NSO manifest that the economy is

expected to stage a resilient V-shaped recovery in H2:2020-21. As per quarterly estimates

released by NSO, the economy has shown a decline of 15.7 per cent by H1: FY 2020-21. A

decline of real GDP by 7.7 per cent for the whole FY:2020-21 indicates a modest decline

of 0.1 per cent in GDP growth in second half of the year. It also indicates a 23.9 per cent

growth in H2: FY2020-21 over H1: FY2020-21. Faster normalisation of business activities

amid gradual lifting of restrictions, higher festive and pent-up demand and policy support

is expected to translate into a faster-than-anticipated economic recovery over the second

half. This is supported by a strong rebound seen in several high frequency indicators in Q3:

FY 2020-21.

1.54 On the demand side, the recovery is expected to be broad-based in the second half

(Figure 42). The biggest growth driver is likely to be government consumption that is

expected to grow at a strong 17 per cent YoY in second half as against a 3.9 per cent

contraction the first half. Private consumption is also expected to improve significantly

with a mild contraction of 0.6 per cent as against a contraction of 18.9 per cent in the first

half. Investment, as measured by Gross Fixed Capital Formation (GFCF), is also expected

to recover significantly with a mild contraction of 0.8 per cent in the second half against a

sharp 29 per cent drop in H1FY21. Net Exports (Exports – Imports) turned positive in the

first half of the year with a larger contraction in imports of 29.1 per cent as compared to

contraction in exports of 10.7 per cent. With gradual recovery of economic activity, both

imports and exports have picked up and net exports is expected to re-enter the negative

territory in the second half. Exports are expected to decline by 5.8 per cent and imports by

11.3 per cent in the second half of the year.