Page 107 - ES 2020-21_Volume-1-2 [28-01-21]

P. 107

90 Economic Survey 2020-21 Volume 1

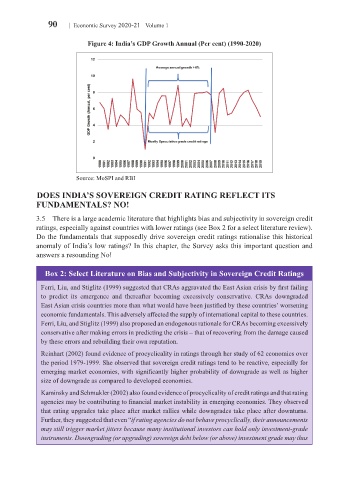

Figure 4: India’s GDP Growth Annual (Per cent) (1990-2020)

Source: MoSPI and RBI

DOES INDIA’S SOVEREIGN CREDIT RATING REFLECT ITS

FUNDAMENTALS? NO!

3.5 There is a large academic literature that highlights bias and subjectivity in sovereign credit

ratings, especially against countries with lower ratings (see Box 2 for a select literature review).

Do the fundamentals that supposedly drive sovereign credit ratings rationalise this historical

anomaly of India’s low ratings? In this chapter, the Survey asks this important question and

answers a resounding No!

Box 2: Select Literature on Bias and Subjectivity in Sovereign Credit Ratings

Ferri, Liu, and Stiglitz (1999) suggested that CRAs aggravated the East Asian crisis by first failing

to predict its emergence and thereafter becoming excessively conservative. CRAs downgraded

East Asian crisis countries more than what would have been justified by these countries’ worsening

economic fundamentals. This adversely affected the supply of international capital to these countries.

Ferri, Liu, and Stiglitz (1999) also proposed an endogenous rationale for CRAs becoming excessively

conservative after making errors in predicting the crisis – that of recovering from the damage caused

by these errors and rebuilding their own reputation.

Reinhart (2002) found evidence of procyclicality in ratings through her study of 62 economies over

the period 1979-1999. She observed that sovereign credit ratings tend to be reactive, especially for

emerging market economies, with significantly higher probability of downgrade as well as higher

size of downgrade as compared to developed economies.

Kaminsky and Schmukler (2002) also found evidence of procyclicality of credit ratings and that rating

agencies may be contributing to financial market instability in emerging economies. They observed

that rating upgrades take place after market rallies while downgrades take place after downturns.

Further, they suggested that even “if rating agencies do not behave procyclically, their announcements

may still trigger market jitters because many institutional investors can hold only investment-grade

instruments. Downgrading (or upgrading) sovereign debt below (or above) investment grade may thus