Page 126 - ES 2020-21_Volume-1-2 [28-01-21]

P. 126

Does India’s Sovereign Credit Rating reflect its fundamentals No! 109

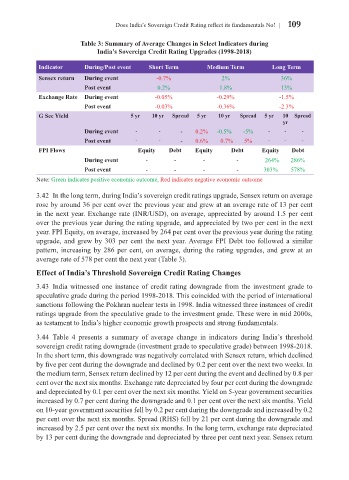

Table 3: Summary of Average Changes in Select Indicators during

India’s Sovereign Credit Rating Upgrades (1998-2018)

Indicator During/Post event Short Term Medium Term Long Term

Sensex return During event -0.7% 2% 36%

Post event 0.2% 1.8% 13%

Exchange Rate During event -0.05% -0.29% -1.5%

Post event -0.03% -0.36% -2.3%

G Sec Yield 5 yr 10 yr Spread 5 yr 10 yr Spread 5 yr 10 Spread

yr

During event - - - 0.2% -0.5% -5% - - -

Post event - - - 0.6% 0.7% 5% - - -

FPI Flows Equity Debt Equity Debt Equity Debt

During event - - - - 264% 286%

Post event - - - - 303% 578%

Note: Green indicates positive economic outcome, Red indicates negative economic outcome

3.42 In the long term, during India’s sovereign credit ratings upgrade, Sensex return on average

rose by around 36 per cent over the previous year and grew at an average rate of 13 per cent

in the next year. Exchange rate (INR/USD), on average, appreciated by around 1.5 per cent

over the previous year during the rating upgrade, and appreciated by two per cent in the next

year. FPI Equity, on average, increased by 264 per cent over the previous year during the rating

upgrade, and grew by 303 per cent the next year. Average FPI Debt too followed a similar

pattern, increasing by 286 per cent, on average, during the rating upgrades, and grew at an

average rate of 578 per cent the next year (Table 3).

Effect of India’s Threshold Sovereign Credit Rating Changes

3.43 India witnessed one instance of credit rating downgrade from the investment grade to

speculative grade during the period 1998-2018. This coincided with the period of international

sanctions following the Pokhran nuclear tests in 1998. India witnessed three instances of credit

ratings upgrade from the speculative grade to the investment grade. These were in mid 2000s,

as testament to India’s higher economic growth prospects and strong fundamentals.

3.44 Table 4 presents a summary of average change in indicators during India’s threshold

sovereign credit rating downgrade (investment grade to speculative grade) between 1998-2018.

In the short term, this downgrade was negatively correlated with Sensex return, which declined

by five per cent during the downgrade and declined by 0.2 per cent over the next two weeks. In

the medium term, Sensex return declined by 12 per cent during the event and declined by 0.8 per

cent over the next six months. Exchange rate depreciated by four per cent during the downgrade

and depreciated by 0.1 per cent over the next six months. Yield on 5-year government securities

increased by 0.7 per cent during the downgrade and 0.1 per cent over the next six months. Yield

on 10-year government securities fell by 0.2 per cent during the downgrade and increased by 0.2

per cent over the next six months. Spread (RHS) fell by 21 per cent during the downgrade and

increased by 2.5 per cent over the next six months. In the long term, exchange rate depreciated

by 13 per cent during the downgrade and depreciated by three per cent next year. Sensex return