Page 207 - ES 2020-21_Volume-1-2 [28-01-21]

P. 207

190 Economic Survey 2020-21 Volume 1

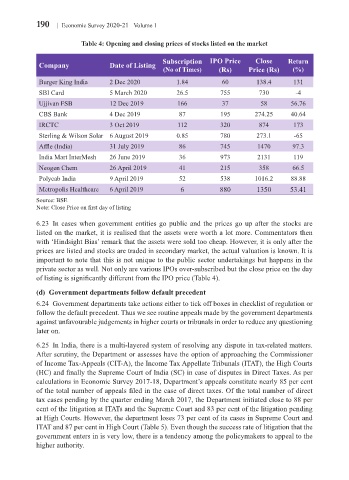

Table 4: Opening and closing prices of stocks listed on the market

Company Date of Listing Subscription IPO Price Close Return

(No of Times) (Rs) Price (Rs) (%)

Burger King India 2 Dec 2020 1.84 60 138.4 131

SBI Card 5 March 2020 26.5 755 730 -4

Ujjivan FSB 12 Dec 2019 166 37 58 56.76

CBS Bank 4 Dec 2019 87 195 274.25 40.64

IRCTC 3 Oct 2019 112 320 874 173

Sterling & Wilson Solar 6 August 2019 0.85 780 273.1 -65

Affle (India) 31 July 2019 86 745 1470 97.3

India Mart InterMesh 26 June 2019 36 973 2131 119

Neogen Chem 26 April 2019 41 215 358 66.5

Polycab India 9 April 2019 52 538 1016.2 88.88

Metropolis Healthcare 6 April 2019 6 880 1350 53.41

Source: BSE

Note: Close Price on first day of listing

6.23 In cases when government entities go public and the prices go up after the stocks are

listed on the market, it is realised that the assets were worth a lot more. Commentators then

with ‘Hindsight Bias’ remark that the assets were sold too cheap. However, it is only after the

prices are listed and stocks are traded in secondary market, the actual valuation is known. It is

important to note that this is not unique to the public sector undertakings but happens in the

private sector as well. Not only are various IPOs over-subscribed but the close price on the day

of listing is significantly different from the IPO price (Table 4).

(d) Government departments follow default precedent

6.24 Government departments take actions either to tick off boxes in checklist of regulation or

follow the default precedent. Thus we see routine appeals made by the government departments

against unfavourable judgements in higher courts or tribunals in order to reduce any questioning

later on.

6.25 In India, there is a multi-layered system of resolving any dispute in tax-related matters.

After scrutiny, the Department or assesses have the option of approaching the Commissioner

of Income Tax-Appeals (CIT-A), the Income Tax Appellate Tribunals (ITAT), the High Courts

(HC) and finally the Supreme Court of India (SC) in case of disputes in Direct Taxes. As per

calculations in Economic Survey 2017-18, Department’s appeals constitute nearly 85 per cent

of the total number of appeals filed in the case of direct taxes. Of the total number of direct

tax cases pending by the quarter ending March 2017, the Department initiated close to 88 per

cent of the litigation at ITATs and the Supreme Court and 83 per cent of the litigation pending

at High Courts. However, the department loses 73 per cent of its cases in Supreme Court and

ITAT and 87 per cent in High Court (Table 5). Even though the success rate of litigation that the

government enters in is very low, there is a tendency among the policymakers to appeal to the

higher authority.