Page 442 - ES 2020-21_Volume-1-2 [28-01-21]

P. 442

Fiscal Developments 69

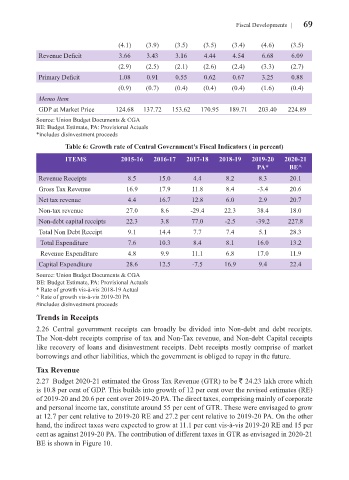

(4.1) (3.9) (3.5) (3.5) (3.4) (4.6) (3.5)

Revenue Deficit 3.66 3.43 3.16 4.44 4.54 6.68 6.09

(2.9) (2.5) (2.1) (2.6) (2.4) (3.3) (2.7)

Primary Deficit 1.08 0.91 0.55 0.62 0.67 3.25 0.88

(0.9) (0.7) (0.4) (0.4) (0.4) (1.6) (0.4)

Memo Item

GDP at Market Price 124.68 137.72 153.62 170.95 189.71 203.40 224.89

Source: Union Budget Documents & CGA

BE: Budget Estimate, PA: Provisional Actuals

*includes disinvestment proceeds

Table 6: Growth rate of Central Government's Fiscal Indicators ( in percent)

ITEMS 2015-16 2016-17 2017-18 2018-19 2019-20 2020-21

PA* BE^

Revenue Receipts 8.5 15.0 4.4 8.2 8.3 20.1

Gross Tax Revenue 16.9 17.9 11.8 8.4 -3.4 20.6

Net tax revenue 4.4 16.7 12.8 6.0 2.9 20.7

Non-tax revenue 27.0 8.6 -29.4 22.3 38.4 18.0

Non-debt capital receipts 22.3 3.8 77.0 -2.5 -39.2 227.8

Total Non Debt Receipt 9.1 14.4 7.7 7.4 5.1 28.3

Total Expenditure 7.6 10.3 8.4 8.1 16.0 13.2

Revenue Expenditure 4.8 9.9 11.1 6.8 17.0 11.9

Capital Expenditure 28.6 12.5 -7.5 16.9 9.4 22.4

Source: Union Budget Documents & CGA

BE: Budget Estimate, PA: Provisional Actuals

* Rate of growth vis-à-vis 2018-19 Actual

^ Rate of growth vis-à-vis 2019-20 PA

#includes disinvestment proceeds

Trends in Receipts

2.26 Central government receipts can broadly be divided into Non-debt and debt receipts.

The Non-debt receipts comprise of tax and Non-Tax revenue, and Non-debt Capital receipts

like recovery of loans and disinvestment receipts. Debt receipts mostly comprise of market

borrowings and other liabilities, which the government is obliged to repay in the future.

Tax Revenue

2.27 Budget 2020-21 estimated the Gross Tax Revenue (GTR) to be ` 24.23 lakh crore which

is 10.8 per cent of GDP. This builds into growth of 12 per cent over the revised estimates (RE)

of 2019-20 and 20.6 per cent over 2019-20 PA. The direct taxes, comprising mainly of corporate

and personal income tax, constitute around 55 per cent of GTR. These were envisaged to grow

at 12.7 per cent relative to 2019-20 RE and 27.2 per cent relative to 2019-20 PA. On the other

hand, the indirect taxes were expected to grow at 11.1 per cent vis-à-vis 2019-20 RE and 15 per

cent as against 2019-20 PA. The contribution of different taxes in GTR as envisaged in 2020-21

BE is shown in Figure 10.