Page 158 - economic_survey_2021-2022

P. 158

132 Economic Survey 2021-22

Timely repayment by the bank to DICGC: To establish the priority of repayment to DICGC

(both interest and principal amount), a provision for penal interest in case of delay has been

put in the act.

No ceiling on premium: The earlier act earlier had a ceiling of 15 paise on premium, which

has been removed. Now, the ceiling on premium will be notified by DICGC, with the prior

approval of RBI.

Since the Act came into force, over `1500 crore has been paid to over 1.2 lakh depositors against their

claims, as of early January 2022.

BANK CREDIT GROWTH

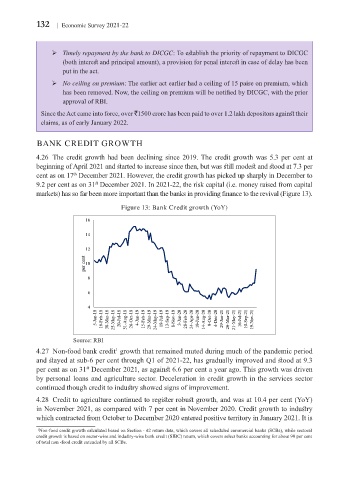

4.26 The credit growth had been declining since 2019. The credit growth was 5.3 per cent at

beginning of April 2021 and started to increase since then, but was still modest and stood at 7.3 per

cent as on 17 December 2021. However, the credit growth has picked up sharply in December to

th

9.2 per cent as on 31 December 2021. In 2021-22, the risk capital (i.e. money raised from capital

st

markets) has so far been more important than the banks in providing finance to the revival (Figure 13).

Figure 13: Bank Credit growth (YoY)

16

14

12

per cent 10

8

6

4

5-Jan-18 16-Feb-18 30-Mar-18 25-May-18 20-Jul-18 31-Aug-18 26-Oct-18 4-Jan-19 15-Feb-19 29-Mar-19 24-May-19 19-Jul-19 13-Sep-19 8-Nov-19 3-Jan-20 28-Feb-20 24-Apr-20 19-Jun-20 14-Aug-20 9-Oct-20 4-Dec-20 29-Jan-21 26-Mar-21 21-May-21 16-Jul-21 10-Sep-21 19-Nov-21

Source: RBI

4.27 Non-food bank credit growth that remained muted during much of the pandemic period

1

and stayed at sub-6 per cent through Q1 of 2021-22, has gradually improved and stood at 9.3

per cent as on 31 December 2021, as against 6.6 per cent a year ago. This growth was driven

st

by personal loans and agriculture sector. Deceleration in credit growth in the services sector

continued though credit to industry showed signs of improvement.

4.28 Credit to agriculture continued to register robust growth, and was at 10.4 per cent (YoY)

in November 2021, as compared with 7 per cent in November 2020. Credit growth to industry

which contracted from October to December 2020 entered positive territory in January 2021. It is

Non-food credit growth calculated based on Section - 42 return data, which covers all scheduled commercial banks (SCBs), while sectoral

1

credit growth is based on sector-wise and industry-wise bank credit (SIBC) return, which covers select banks accounting for about 90 per cent

of total non -food credit extended by all SCBs.