Page 393 - ES 2020-21_Volume-1-2 [28-01-21]

P. 393

20 Economic Survey 2020-21 Volume 2

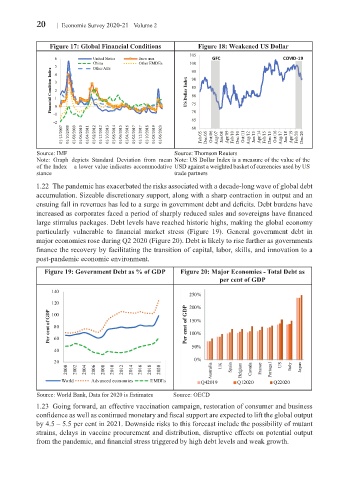

Figure 17: Global Financial Conditions Figure 18: Weakened uS Dollar

105

6 United States Euro area GFC COVID-19

China Other EMDEs 100

5 4 Other AEs 95

Financial Condition Index 3 2 1 US Dollar Index 90

85

80

75

0

70

-1

65

-2 60

01/12/2007 01/10/2008 01/08/2009 01/06/2010 01/04/2011 01/02/2012 01/12/2012 01/10/2013 01/08/2014 01/06/2015 01/04/2016 01/02/2017 01/12/2017 01/10/2018 01/08/2019 01/06/2020 Feb/05 Dec/05 Oct/06 Aug/07 Jun/08 Apr/09 Feb/10 Dec/10 Oct/11 Aug/12 Jun/13 Apr/14 Feb/15 Dec/15 Oct/16 Aug/17 Jun/18 Apr/19 Feb/20 Dec/20

Source: IMF Source: Thomson Reuters

Note: Graph depicts Standard Deviation from mean Note: US Dollar Index is a measure of the value of the

of the Index – a lower value indicates accommodative USD against a weighted basket of currencies used by US

stance trade partners

1.22 The pandemic has exacerbated the risks associated with a decade-long wave of global debt

accumulation. Sizeable discretionary support, along with a sharp contraction in output and an

ensuing fall in revenues has led to a surge in government debt and deficits. Debt burdens have

increased as corporates faced a period of sharply reduced sales and sovereigns have financed

large stimulus packages. Debt levels have reached historic highs, making the global economy

particularly vulnerable to financial market stress (Figure 19). General government debt in

major economies rose during Q2 2020 (Figure 20). Debt is likely to rise further as governments

finance the recovery by facilitating the transition of capital, labor, skills, and innovation to a

post-pandemic economic environment.

Figure 19: Government Debt as % of GDP Figure 20: Major Economies - Total Debt as

per cent of GDP

Source: World Bank, Data for 2020 is Estimates Source: OECD

1.23 Going forward, an effective vaccination campaign, restoration of consumer and business

confidence as well as continued monetary and fiscal support are expected to lift the global output

by 4.5 – 5.5 per cent in 2021. Downside risks to this forecast include the possibility of mutant

strains, delays in vaccine procurement and distribution, disruptive effects on potential output

from the pandemic, and financial stress triggered by high debt levels and weak growth.