Page 449 - ES 2020-21_Volume-1-2 [28-01-21]

P. 449

76 Economic Survey 2020-21 Volume 2

2.42 Central government debt is characterised by low currency and interest rate risks. This is

owing to low share of external debt in the debt portfolio and almost entire external borrowings

being from official sources. Further, most of the public debt has been contracted at fixed interest

rate making India’s debt stock virtually insulated from interest rate volatility. This lends certainty

and stability to budget in terms of interest payments.

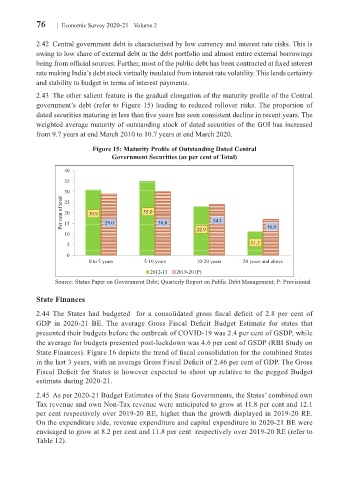

2.43 The other salient feature is the gradual elongation of the maturity profile of the Central

government’s debt (refer to Figure 15) leading to reduced rollover risks. The proportion of

dated securities maturing in less than five years has seen consistent decline in recent years. The

weighted average maturity of outstanding stock of dated securities of the GOI has increased

from 9.7 years at end March 2010 to 10.7 years at end March 2020.

Figure 15: Maturity Profile of Outstanding Dated Central

Government Securities (as per cent of Total)

40

35

30

Per cent of total 20 30.9 29.0 35.0 30.0 24.1

25

15

10 22.9 16.9

5 11.2

0

0 to 5 years 5-10 years 10-20 years 20 years and above

2012-13 2019-20 (P)

Source: Status Paper on Government Debt; Quarterly Report on Public Debt Management; P: Provisional

State Finances

2.44 The States had budgeted for a consolidated gross fiscal deficit of 2.8 per cent of

GDP in 2020-21 BE. The average Gross Fiscal Deficit Budget Estimate for states that

presented their budgets before the outbreak of COVID-19 was 2.4 per cent of GSDP, while

the average for budgets presented post-lockdown was 4.6 per cent of GSDP (RBI Study on

State Finances). Figure 16 depicts the trend of fiscal consolidation for the combined States

in the last 3 years, with an average Gross Fiscal Deficit of 2.46 per cent of GDP. The Gross

Fiscal Deficit for States is however expected to shoot up relative to the pegged Budget

estimate during 2020-21.

2.45 As per 2020-21 Budget Estimates of the State Governments, the States’ combined own

Tax revenue and own Non-Tax revenue were anticipated to grow at 11.8 per cent and 12.1

per cent respectively over 2019-20 RE, higher than the growth displayed in 2019-20 RE.

On the expenditure side, revenue expenditure and capital expenditure in 2020-21 BE were

envisaged to grow at 8.2 per cent and 11.8 per cent respectively over 2019-20 RE (refer to

Table 12).