Page 34 - economic_survey_2021-2022

P. 34

8 Economic Survey 2021-22

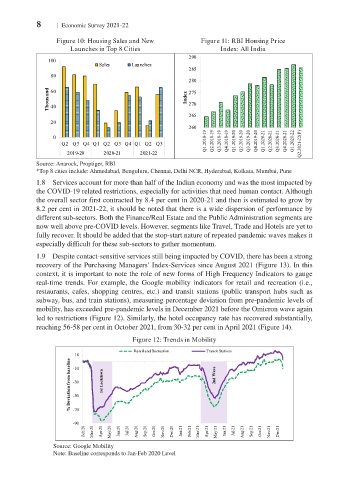

Figure 10: Housing Sales and New Figure 11: RBI Housing Price

Launches in Top 8 Cities Index: All India

290

100

Sales Launches

285

80

280

Thousand 60 Index 275

270

40

265

20

260

0

Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q1.2018-19 Q2.2018-19 Q3.2018-19 Q4.2018-19 Q1.2019-20 Q2.2019-20 Q3.2019-20 Q4.2019-20 Q1.2020-21 Q2.2020-21 Q3.2020-21 Q4.2020-21 Q1.2021-22 Q2.2021-22(P)

2019-20 2020-21 2021-22

Source: Anarock, Proptiger, RBI

*Top 8 cities include: Ahmedabad, Benguluru, Chennai, Delhi NCR, Hyderabad, Kolkata, Mumbai, Pune

1.8 Services account for more than half of the Indian economy and was the most impacted by

the COVID-19 related restrictions, especially for activities that need human contact. Although

the overall sector first contracted by 8.4 per cent in 2020-21 and then is estimated to grow by

8.2 per cent in 2021-22, it should be noted that there is a wide dispersion of performance by

different sub-sectors. Both the Finance/Real Estate and the Public Administration segments are

now well above pre-COVID levels. However, segments like Travel, Trade and Hotels are yet to

fully recover. It should be added that the stop-start nature of repeated pandemic waves makes it

especially difficult for these sub-sectors to gather momentum.

1.9 Despite contact-sensitive services still being impacted by COVID, there has been a strong

recovery of the Purchasing Managers’ Index-Services since August 2021 (Figure 13). In this

context, it is important to note the role of new forms of High Frequency Indicators to gauge

real-time trends. For example, the Google mobility indicators for retail and recreation (i.e.,

restaurants, cafes, shopping centres, etc.) and transit stations (public transport hubs such as

subway, bus, and train stations), measuring percentage deviation from pre-pandemic levels of

mobility, has exceeded pre-pandemic levels in December 2021 before the Omicron wave again

led to restrictions (Figure 12). Similarly, the hotel occupancy rate has recovered substantially,

reaching 56-58 per cent in October 2021, from 30-32 per cent in April 2021 (Figure 14).

Figure 12: Trends in Mobility

Retail and Recreation Transit Stations

10

% Deviation from baseline -30 1st Lockdown 2nd Wave

-10

-50

-70

-90

Feb/20 Mar/20 Apr/20 May/20 Jun/20 Jul/20 Aug/20 Sep/20 Oct/20 Nov/20 Dec/20 Jan/21 Feb/21 Mar/21 Apr/21 May/21 Jun/21 Jul/21 Aug/21 Sep/21 Oct/21 Nov/21 Dec/21

Source: Google Mobility

Note: Baseline corresponds to Jan-Feb 2020 Level