Page 223 - ES 2020-21_Volume-1-2 [28-01-21]

P. 223

206 Economic Survey 2020-21 Volume 1

otherwise similar, any difference in their propensity to restructuring could be attributed to

their varying susceptibility to exploiting forbearance. With this strategy for identification of

the causal effects, the lending activity of banks over the years 2002-2015 is analyzed. The

years are split into three groups: the pre-forbearance period of 2002-2008, the crisis period of

2009-2011, and the post-crisis period of 2011-2015. Organizing the data at a firm-bank-year

level, the following regression is estimated:

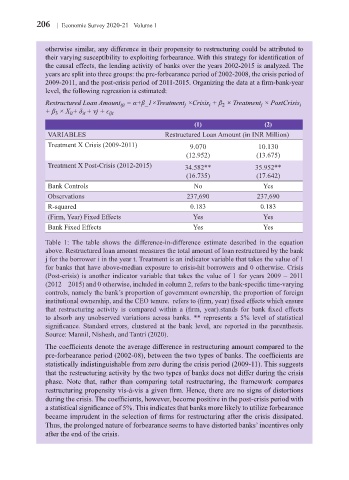

Restructured Loan Amount = α+β_1×Treatment ×Crisis + β × Treatment × PostCrisis

j

ijt

t

t

j

2

+ β × X + δ + νj + ϵ ijt

it

it

3

(1) (2)

VARIABLES Restructured Loan Amount (in INR Million)

Treatment X Crisis (2009-2011) 9.070 10.130

(12.952) (13.675)

Treatment X Post-Crisis (2012-2015) 34.582** 35.952**

(16.735) (17.642)

Bank Controls No Yes

Observations 237,690 237,690

R-squared 0.183 0.183

(Firm, Year) Fixed Effects Yes Yes

Bank Fixed Effects Yes Yes

Table 1: The table shows the difference-in-difference estimate described in the equation

above. Restructured loan amount measures the total amount of loan restructured by the bank

j for the borrower i in the year t. Treatment is an indicator variable that takes the value of 1

for banks that have above-median exposure to crisis-hit borrowers and 0 otherwise. Crisis

(Post-crisis) is another indicator variable that takes the value of 1 for years 2009 – 2011

(2012 – 2015) and 0 otherwise, included in column 2, refers to the bank-specific time-varying

controls, namely the bank’s proportion of government ownership, the proportion of foreign

institutional ownership, and the CEO tenure. refers to (firm, year) fixed effects which ensure

that restructuring activity is compared within a (firm, year).stands for bank fixed effects

to absorb any unobserved variations across banks. ** represents a 5% level of statistical

significance. Standard errors, clustered at the bank level, are reported in the parenthesis.

Source: Mannil, Nishesh, and Tantri (2020).

The coefficients denote the average difference in restructuring amount compared to the

pre-forbearance period (2002-08), between the two types of banks. The coefficients are

statistically indistinguishable from zero during the crisis period (2009-11). This suggests

that the restructuring activity by the two types of banks does not differ during the crisis

phase. Note that, rather than comparing total restructuring, the framework compares

restructuring propensity vis-à-vis a given firm. Hence, there are no signs of distortions

during the crisis. The coefficients, however, become positive in the post-crisis period with

a statistical significance of 5%. This indicates that banks more likely to utilize forbearance

became imprudent in the selection of firms for restructuring after the crisis dissipated.

Thus, the prolonged nature of forbearance seems to have distorted banks’ incentives only

after the end of the crisis.