Page 218 - ES 2020-21_Volume-1-2 [28-01-21]

P. 218

Regulatory Forbearance: An Emergency Medicine, Not Staple Diet! 201

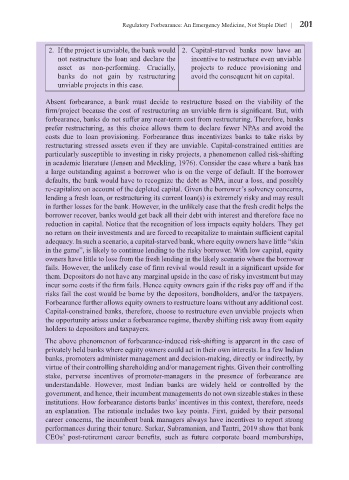

2. If the project is unviable, the bank would 2. Capital-starved banks now have an

not restructure the loan and declare the incentive to restructure even unviable

asset as non-performing. Crucially, projects to reduce provisioning and

banks do not gain by restructuring avoid the consequent hit on capital.

unviable projects in this case.

Absent forbearance, a bank must decide to restructure based on the viability of the

firm/project because the cost of restructuring an unviable firm is significant. But, with

forbearance, banks do not suffer any near-term cost from restructuring. Therefore, banks

prefer restructuring, as this choice allows them to declare fewer NPAs and avoid the

costs due to loan provisioning. Forbearance thus incentivizes banks to take risks by

restructuring stressed assets even if they are unviable. Capital-constrained entities are

particularly susceptible to investing in risky projects, a phenomenon called risk-shifting

in academic literature (Jensen and Meckling, 1976). Consider the case where a bank has

a large outstanding against a borrower who is on the verge of default. If the borrower

defaults, the bank would have to recognize the debt as NPA, incur a loss, and possibly

re-capitalize on account of the depleted capital. Given the borrower’s solvency concerns,

lending a fresh loan, or restructuring its current loan(s) is extremely risky and may result

in further losses for the bank. However, in the unlikely case that the fresh credit helps the

borrower recover, banks would get back all their debt with interest and therefore face no

reduction in capital. Notice that the recognition of loss impacts equity holders. They get

no return on their investments and are forced to recapitalize to maintain sufficient capital

adequacy. In such a scenario, a capital-starved bank, where equity owners have little “skin

in the game”, is likely to continue lending to the risky borrower. With low capital, equity

owners have little to lose from the fresh lending in the likely scenario where the borrower

fails. However, the unlikely case of firm revival would result in a significant upside for

them. Depositors do not have any marginal upside in the case of risky investment but may

incur some costs if the firm fails. Hence equity owners gain if the risks pay off and if the

risks fail the cost would be borne by the depositors, bondholders, and/or the taxpayers.

Forbearance further allows equity owners to restructure loans without any additional cost.

Capital-constrained banks, therefore, choose to restructure even unviable projects when

the opportunity arises under a forbearance regime, thereby shifting risk away from equity

holders to depositors and taxpayers.

The above phenomenon of forbearance-induced risk-shifting is apparent in the case of

privately held banks where equity owners could act in their own interests. In a few Indian

banks, promoters administer management and decision-making, directly or indirectly, by

virtue of their controlling shareholding and/or management rights. Given their controlling

stake, perverse incentives of promoter-managers in the presence of forbearance are

understandable. However, most Indian banks are widely held or controlled by the

government, and hence, their incumbent managements do not own sizeable stakes in these

institutions. How forbearance distorts banks’ incentives in this context, therefore, needs

an explanation. The rationale includes two key points. First, guided by their personal

career concerns, the incumbent bank managers always have incentives to report strong

performances during their tenure. Sarkar, Subramanian, and Tantri, 2019 show that bank

CEOs’ post-retirement career benefits, such as future corporate board memberships,