Page 497 - ES 2020-21_Volume-1-2 [28-01-21]

P. 497

124 Economic Survey 2020-21 Volume 1

and the December 2020 meetings were held as per schedule, while the October meeting was

postponed by a week as new external members were onboarded to the MPC. Since March

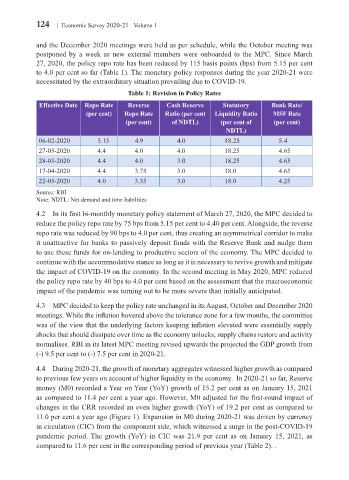

27, 2020, the policy repo rate has been reduced by 115 basis points (bps) from 5.15 per cent

to 4.0 per cent so far (Table 1). The monetary policy responses during the year 2020-21 were

necessitated by the extraordinary situation prevailing due to COVID-19.

Table 1: Revision in Policy Rates

Effective Date Repo Rate Reverse Cash Reserve Statutory Bank Rate/

(per cent) Repo Rate Ratio (per cent Liquidity Ratio MSF Rate

(per cent) of NDTL) (per cent of (per cent)

NDTL)

06-02-2020 5.15 4.9 4.0 18.25 5.4

27-03-2020 4.4 4.0 4.0 18.25 4.65

28-03-2020 4.4 4.0 3.0 18.25 4.65

17-04-2020 4.4 3.75 3.0 18.0 4.65

22-05-2020 4.0 3.35 3.0 18.0 4.25

Source: RBI

Note: NDTL: Net demand and time liabilities

4.2 In its first bi-monthly monetary policy statement of March 27, 2020, the MPC decided to

reduce the policy repo rate by 75 bps from 5.15 per cent to 4.40 per cent. Alongside, the reverse

repo rate was reduced by 90 bps to 4.0 per cent, thus creating an asymmetrical corridor to make

it unattractive for banks to passively deposit funds with the Reserve Bank and nudge them

to use these funds for on-lending to productive sectors of the economy. The MPC decided to

continue with the accommodative stance as long as it is necessary to revive growth and mitigate

the impact of COVID-19 on the economy. In the second meeting in May 2020, MPC reduced

the policy repo rate by 40 bps to 4.0 per cent based on the assessment that the macroeconomic

impact of the pandemic was turning out to be more severe than initially anticipated.

4.3 MPC decided to keep the policy rate unchanged in its August, October and December 2020

meetings. While the inflation hovered above the tolerance zone for a few months, the committee

was of the view that the underlying factors keeping inflation elevated were essentially supply

shocks that should dissipate over time as the economy unlocks, supply chains restore and activity

normalises. RBI in its latest MPC meeting revised upwards the projected the GDP growth from

(-) 9.5 per cent to (-) 7.5 per cent in 2020-21.

4.4 During 2020-21, the growth of monetary aggregates witnessed higher growth as compared

to previous few years on account of higher liquidity in the economy. In 2020-21 so far, Reserve

money (M0) recorded a Year on Year (YoY) growth of 15.2 per cent as on January 15, 2021

as compared to 11.4 per cent a year ago. However, M0 adjusted for the first-round impact of

changes in the CRR recorded an even higher growth (YoY) of 19.2 per cent as compared to

11.0 per cent a year ago (Figure 1). Expansion in M0 during 2020-21 was driven by currency

in circulation (CIC) from the component side, which witnessed a surge in the post-COVID-19

pandemic period. The growth (YoY) in CIC was 21.9 per cent as on January 15, 2021, as

compared to 11.6 per cent in the corresponding period of previous year (Table 2). .