Page 502 - ES 2020-21_Volume-1-2 [28-01-21]

P. 502

Monetary Management and Financial Intermediation 129

4.12 The increased government spending during April-May 2020 also added to the liquidity

surplus. However, the Government’s cash balances turned into surplus in June 2020 and July

2020. In Q2 of 2020, although surplus liquidity conditions still existed, there was moderation as

compared to Q1. As a result, average daily net absorption under the LAF decreased to ` 3.95 lakh

crore in July 2020 as average Government cash surplus increased to ` 95,942 crore. Thereafter,

daily net absorption increased to ` 4.03 lakh crore in August 2020, which again moderated to

` 3.68 lakh crore in September 2020. This moderation could be attributed to the absorption of

banking sector liquidity to the tune of ` 1.24 lakh crore under the option given to banks to return

the funds availed under LTRO facility before maturity. The moderation in liquidity absorption,

however, was reversed in following months as average daily net absorption under the LAF again

increased to ` 4.47 lakh crore and ` 5.64 lakh crore in the month of October and November 2020.

This is partly a reflection of pick up in government spending.

4.13 In order to ensure better monetary transmission through a more even distribution of

liquidity across tenors, 14 simultaneous sale-purchase OMO auctions for ` 10,000 crore each

were conducted in the financial year 2020-21

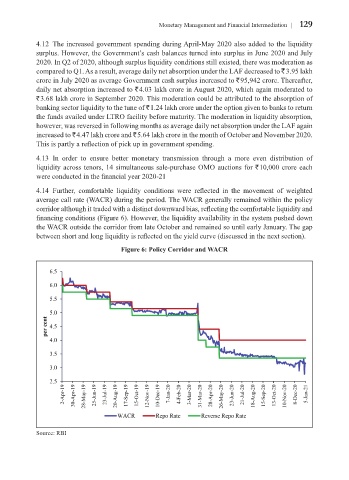

4.14 Further, comfortable liquidity conditions were reflected in the movement of weighted

average call rate (WACR) during the period. The WACR generally remained within the policy

corridor although it traded with a distinct downward bias, reflecting the comfortable liquidity and

financing conditions (Figure 6). However, the liquidity availability in the system pushed down

the WACR outside the corridor from late October and remained so until early January. The gap

between short and long liquidity is reflected on the yield curve (discussed in the next section).

Figure 6: Policy Corridor and WACR

Source: RBI