Page 503 - ES 2020-21_Volume-1-2 [28-01-21]

P. 503

130 Economic Survey 2020-21 Volume 1

DEVELOPMENTS IN THE G-SEC MARKETS

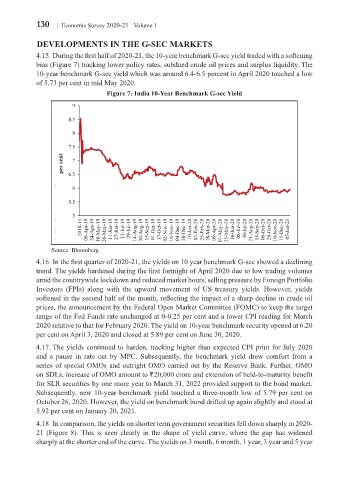

4.15. During the first half of 2020-21, the 10-year benchmark G-sec yield traded with a softening

bias (Figure 7) tracking lower policy rates, subdued crude oil prices and surplus liquidity. The

10-year benchmark G-sec yield which was around 6.4-6.5 percent in April 2020 touched a low

of 5.73 per cent in mid May 2020.

Figure 7: India 10-Year Benchmark G-sec Yield

Source: Bloomberg.

4.16 In the first quarter of 2020-21, the yields on 10 year benchmark G-sec showed a declining

trend. The yields hardened during the first fortnight of April 2020 due to low trading volumes

amid the countrywide lockdown and reduced market hours, selling pressure by Foreign Portfolio

Investors (FPIs) along with the upward movement of US treasury yields. However, yields

softened in the second half of the month, reflecting the impact of a sharp decline in crude oil

prices, the announcement by the Federal Open Market Committee (FOMC) to keep the target

range of the Fed Funds rate unchanged at 0-0.25 per cent and a lower CPI reading for March

2020 relative to that for February 2020. The yield on 10-year benchmark security opened at 6.20

per cent on April 3, 2020 and closed at 5.89 per cent on June 30, 2020.

4.17. The yields continued to harden, tracking higher than expected CPI print for July 2020

and a pause in rate cut by MPC. Subsequently, the benchmark yield drew comfort from a

series of special OMOs and outright OMO carried out by the Reserve Bank. Further, OMO

on SDLs, increase of OMO amount to ` 20,000 crore and extension of held-to-maturity benefit

for SLR securities by one more year to March 31, 2022 provided support to the bond market.

Subsequently, new 10-year benchmark yield touched a three-month low of 5.79 per cent on

October 26, 2020. However, the yield on benchmark bond drifted up again slightly and stood at

5.92 per cent on January 20, 2021.

4.18 In comparison, the yields on shorter term government securities fell down sharply in 2020-

21 (Figure 8). This is seen clearly in the shape of yield curve, where the gap has widened

sharply at the shorter end of the curve. The yields on 3 month, 6 month, 1 year, 3 year and 5 year