Page 504 - ES 2020-21_Volume-1-2 [28-01-21]

P. 504

Monetary Management and Financial Intermediation 131

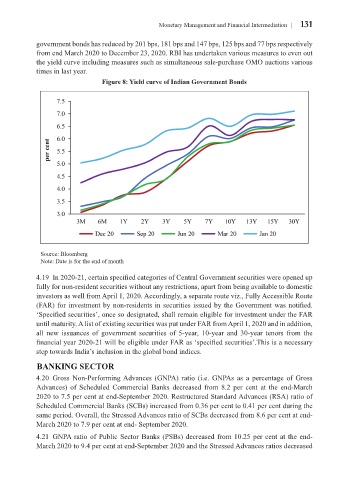

government bonds has reduced by 201 bps, 181 bps and 147 bps, 125 bps and 77 bps respectively

from end March 2020 to December 23, 2020. RBI has undertaken various measures to even out

the yield curve including measures such as simultaneous sale-purchase OMO auctions various

times in last year.

Figure 8: Yield curve of Indian Government Bonds

Source: Bloomberg

Note: Date is for the end of month

4.19 In 2020-21, certain specified categories of Central Government securities were opened up

fully for non-resident securities without any restrictions, apart from being available to domestic

investors as well from April 1, 2020. Accordingly, a separate route viz., Fully Accessible Route

(FAR) for investment by non-residents in securities issued by the Government was notified.

‘Specified securities’, once so designated, shall remain eligible for investment under the FAR

until maturity. A list of existing securities was put under FAR from April 1, 2020 and in addition,

all new issuances of government securities of 5-year, 10-year and 30-year tenors from the

financial year 2020-21 will be eligible under FAR as ‘specified securities’.This is a necessary

step towards India’s inclusion in the global bond indices.

BANKING SECTOR

4.20 Gross Non-Performing Advances (GNPA) ratio (i.e. GNPAs as a percentage of Gross

Advances) of Scheduled Commercial Banks decreased from 8.2 per cent at the end-March

2020 to 7.5 per cent at end-September 2020. Restructured Standard Advances (RSA) ratio of

Scheduled Commercial Banks (SCBs) increased from 0.36 per cent to 0.41 per cent during the

same period. Overall, the Stressed Advances ratio of SCBs decreased from 8.6 per cent at end-

March 2020 to 7.9 per cent at end- September 2020.

4.21 GNPA ratio of Public Sector Banks (PSBs) decreased from 10.25 per cent at the end-

March 2020 to 9.4 per cent at end-September 2020 and the Stressed Advances ratios decreased