Page 505 - ES 2020-21_Volume-1-2 [28-01-21]

P. 505

132 Economic Survey 2020-21 Volume 1

from 10.75 per cent to 9.96 per cent during the same period. Net NPA ratios also declined and

stood at 2.1 per cent for SCBs and 2.85 per cent for PSBs as at end- September 2020.

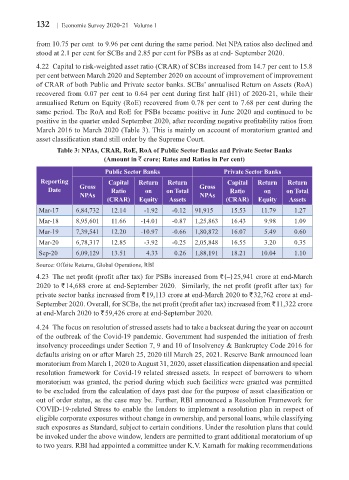

4.22 Capital to risk-weighted asset ratio (CRAR) of SCBs increased from 14.7 per cent to 15.8

per cent between March 2020 and September 2020 on account of improvement of improvement

of CRAR of both Public and Private sector banks. SCBs’ annualised Return on Assets (RoA)

recovered from 0.07 per cent to 0.64 per cent during first half (H1) of 2020-21, while their

annualised Return on Equity (RoE) recovered from 0.78 per cent to 7.68 per cent during the

same period. The RoA and RoE for PSBs became positive in June 2020 and continued to be

positive in the quarter ended September 2020, after recording negative profitability ratios from

March 2016 to March 2020 (Table 3). This is mainly on account of moratorium granted and

asset classification stand still order by the Supreme Court.

Table 3: NPAs, CRAR, RoE, RoA of Public Sector Banks and Private Sector Banks

(Amount in ` crore; Rates and Ratios in Per cent)

Public Sector Banks Private Sector Banks

Reporting Capital Return Return Capital Return Return

Date Gross Ratio on on Total Gross Ratio on on Total

NPAs NPAs

(CRAR) Equity Assets (CRAR) Equity Assets

Mar-17 6,84,732 12.14 -1.92 -0.12 91,915 15.53 11.79 1.27

Mar-18 8,95,601 11.66 -14.01 -0.87 1,25,863 16.43 9.98 1.09

Mar-19 7,39,541 12.20 -10.97 -0.66 1,80,872 16.07 5.49 0.60

Mar-20 6,78,317 12.85 -3.92 -0.25 2,05,848 16.55 3.20 0.35

Sep-20 6,09,129 13.51 4.33 0.26 1,88,191 18.21 10.04 1.10

Source: Offsite Returns, Global Operations, RBI

4.23 The net profit (profit after tax) for PSBs increased from ` (–) 25,941 crore at end-March

2020 to ` 14,688 crore at end-September 2020. Similarly, the net profit (profit after tax) for

private sector banks increased from ` 19,113 crore at end-March 2020 to ` 32,762 crore at end-

September 2020. Overall, for SCBs, the net profit (profit after tax) increased from ` 11,322 crore

at end-March 2020 to ` 59,426 crore at end-September 2020.

4.24 The focus on resolution of stressed assets had to take a backseat during the year on account

of the outbreak of the Covid-19 pandemic. Government had suspended the initiation of fresh

insolvency proceedings under Section 7, 9 and 10 of Insolvency & Bankruptcy Code 2016 for

defaults arising on or after March 25, 2020 till March 25, 2021. Reserve Bank announced loan

moratorium from March 1, 2020 to August 31, 2020, asset classification dispensation and special

resolution framework for Covid-19 related stressed assets. In respect of borrowers to whom

moratorium was granted, the period during which such facilities were granted was permitted

to be excluded from the calculation of days past due for the purpose of asset classification or

out of order status, as the case may be. Further, RBI announced a Resolution Framework for

COVID-19-related Stress to enable the lenders to implement a resolution plan in respect of

eligible corporate exposures without change in ownership, and personal loans, while classifying

such exposures as Standard, subject to certain conditions. Under the resolution plans that could

be invoked under the above window, lenders are permitted to grant additional moratorium of up

to two years. RBI had appointed a committee under K.V. Kamath for making recommendations