Page 506 - ES 2020-21_Volume-1-2 [28-01-21]

P. 506

Monetary Management and Financial Intermediation 133

on the required financial parameters to be factored in resolution plans. Also, MSME accounts

classified as Standard where the aggregate exposure of banks and NBFCs was ` 25 crore or

below as on March 1, 2020, were permitted to be restructured without a downgrade in the

asset classification, subject to certain conditions. Notably, the Supreme Court issued an interim

order dated September 3, 2020 specifying that “the accounts which were not declared NPA till

31.08.2020 shall not be declared NPA till further orders”.

4.25 The above measures, which provided asset classification reliefs to borrowers, would affect

the true recognition of financial stress on the borrower accounts. However, the larger objective

of financial stability in the wake of pandemic demanded prudential forbearance which was

exercised through clear boundaries and disincentives embedded in the above reliefs. Moreover,

the risk recognition has not been completely suspended as the lenders are required to make

provisions of at least 10 per cent in respect of accounts which availed of asset classification

benefits under the above reliefs.

MONETARY POLICY TRANSMISSION

4.26 RBI has reduced repo rate by 250 bps since February 2019 (the current easing cycle). The

transmission of policy repo rate changes has been weak on quantity of credit. However, there

has been improved transmission on rate structure and term structure.

a. Rate structure

4.27 The transmission of policy repo rate changes to deposit and lending rates of scheduled

commercial banks (SCBs) has improved since March 2020 reflecting the combined impact of

policy rate cuts, large liquidity surplus with accommodative policy stance, and the introduction

of external benchmark-based pricing of loans. The weighted average lending rate (WALR) on

fresh rupee loans declined by 94 bps between March 2020 and November 2020 in response to the

reduction of 115 bps in the policy repo rate and comfortable liquidity conditions. In the current

easing phase (February 2019 to November 2020), the change in the WALR on outstanding rupee

loans has shown significant improvement since March 2020. Of the 83-bps decline in WALR on

outstanding loans in February 2019 to November 2020 period, 67 bps decline was noted since

March 2020. The weighted average domestic term deposit rate (WADTDR) on outstanding rupee

deposits declined by 127 bps during the ongoing easing cycle. The median term deposit rate has

registered a sizable decline of 146 bps in March to December 2020 (Table 4). The spread between

WALR on outstanding loans and repo rate which was increasing since 2018 started to decline in

2020-21. However, WALR on outstanding loans is still 544 bps higher than repo rate (Figure 9).

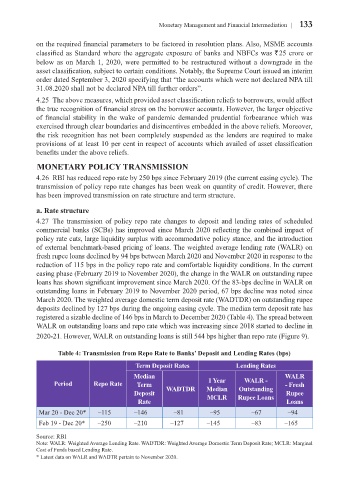

Table 4: Transmission from Repo Rate to Banks’ Deposit and Lending Rates (bps)

Term Deposit Rates Lending Rates

Median WALR

Period Repo Rate Term 1 Year WALR - - Fresh

Outstanding

Deposit WADTDR Median Rupee Loans Rupee

MCLR

Rate Loans

Mar 20 - Dec 20* –115 –146 –81 –95 –67 –94

Feb 19 - Dec 20* –250 –210 –127 –145 –83 –165

Source: RBI

Note: WALR: Weighted Average Lending Rate. WADTDR: Weighted Average Domestic Term Deposit Rate; MCLR: Marginal

Cost of Funds based Lending Rate.

* Latest data on WALR and WADTR pertain to November 2020.