Page 509 - ES 2020-21_Volume-1-2 [28-01-21]

P. 509

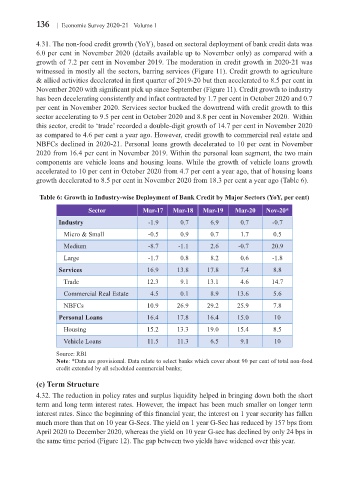

136 Economic Survey 2020-21 Volume 1

4.31. The non-food credit growth (YoY), based on sectoral deployment of bank credit data was

6.0 per cent in November 2020 (details available up to November only) as compared with a

growth of 7.2 per cent in November 2019. The moderation in credit growth in 2020-21 was

witnessed in mostly all the sectors, barring services (Figure 11). Credit growth to agriculture

& allied activities decelerated in first quarter of 2019-20 but then accelerated to 8.5 per cent in

November 2020 with significant pick up since September (Figure 11). Credit growth to industry

has been decelerating consistently and infact contracted by 1.7 per cent in October 2020 and 0.7

per cent in November 2020. Services sector bucked the downtrend with credit growth to this

sector accelerating to 9.5 per cent in October 2020 and 8.8 per cent in November 2020. Within

this sector, credit to ‘trade’ recorded a double-digit growth of 14.7 per cent in November 2020

as compared to 4.6 per cent a year ago. However, credit growth to commercial real estate and

NBFCs declined in 2020-21. Personal loans growth decelerated to 10 per cent in November

2020 from 16.4 per cent in November 2019. Within the personal loan segment, the two main

components are vehicle loans and housing loans. While the growth of vehicle loans growth

accelerated to 10 per cent in October 2020 from 4.7 per cent a year ago, that of housing loans

growth decelerated to 8.5 per cent in November 2020 from 18.3 per cent a year ago (Table 6).

Table 6: Growth in Industry-wise Deployment of Bank Credit by Major Sectors (YoY, per cent)

Sector Mar-17 Mar-18 Mar-19 Mar-20 Nov-20*

Industry -1.9 0.7 6.9 0.7 -0.7

Micro & Small -0.5 0.9 0.7 1.7 0.5

Medium -8.7 -1.1 2.6 -0.7 20.9

Large -1.7 0.8 8.2 0.6 -1.8

Services 16.9 13.8 17.8 7.4 8.8

Trade 12.3 9.1 13.1 4.6 14.7

Commercial Real Estate 4.5 0.1 8.9 13.6 5.6

NBFCs 10.9 26.9 29.2 25.9 7.8

Personal Loans 16.4 17.8 16.4 15.0 10

Housing 15.2 13.3 19.0 15.4 8.5

Vehicle Loans 11.5 11.3 6.5 9.1 10

Source: RBI

Note: *Data are provisional. Data relate to select banks which cover about 90 per cent of total non-food

credit extended by all scheduled commercial banks;

(c) Term Structure

4.32. The reduction in policy rates and surplus liquidity helped in bringing down both the short

term and long term interest rates. However, the impact has been much smaller on longer term

interest rates. Since the beginning of this financial year, the interest on 1 year security has fallen

much more than that on 10 year G-Secs. The yield on 1 year G-Sec has reduced by 157 bps from

April 2020 to December 2020, whereas the yield on 10 year G-sec has declined by only 24 bps in

the same time period (Figure 12). The gap between two yields have widened over this year.