Page 498 - ES 2020-21_Volume-1-2 [28-01-21]

P. 498

Monetary Management and Financial Intermediation 125

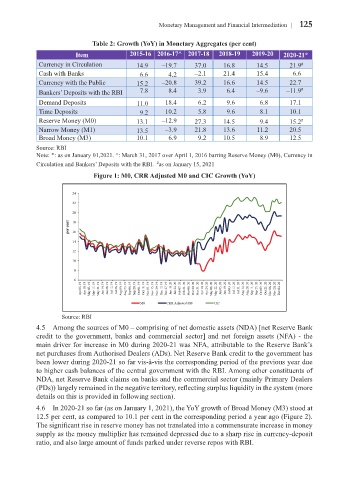

Table 2: Growth (YoY) in Monetary Aggregates (per cent)

Item 2015-16 2016-17^ 2017-18 2018-19 2019-20 2020-21*

Currency in Circulation 14.9 –19.7 37.0 16.8 14.5 21.9 #

Cash with Banks 6.6 4.2 –2.1 21.4 15.4 6.6

Currency with the Public 15.2 –20.8 39.2 16.6 14.5 22.7

Bankers’ Deposits with the RBI 7.8 8.4 3.9 6.4 –9.6 –11.9 #

Demand Deposits 11.0 18.4 6.2 9.6 6.8 17.1

Time Deposits 9.2 10.2 5.8 9.6 8.1 10.1

Reserve Money (M0) 13.1 –12.9 27.3 14.5 9.4 15.2 #

Narrow Money (M1) 13.5 –3.9 21.8 13.6 11.2 20.5

Broad Money (M3) 10.1 6.9 9.2 10.5 8.9 12.5

Source: RBI

Note: *: as on January 01,2021. ^: March 31, 2017 over April 1, 2016 barring Reserve Money (M0), Currency in

#

Circulation and Bankers’ Deposits with the RBI. as on January 15, 2021

Figure 1: M0, CRR Adjusted M0 and CIC Growth (YoY)

Source: RBI

4.5 Among the sources of M0 – comprising of net domestic assets (NDA) [net Reserve Bank

credit to the government, banks and commercial sector] and net foreign assets (NFA) - the

main driver for increase in M0 during 2020-21 was NFA, attributable to the Reserve Bank’s

net purchases from Authorised Dealers (ADs). Net Reserve Bank credit to the government has

been lower during 2020-21 so far vis-à-vis the corresponding period of the previous year due

to higher cash balances of the central government with the RBI. Among other constituents of

NDA, net Reserve Bank claims on banks and the commercial sector (mainly Primary Dealers

(PDs)) largely remained in the negative territory, reflecting surplus liquidity in the system (more

details on this is provided in following section).

4.6 In 2020-21 so far (as on January 1, 2021), the YoY growth of Broad Money (M3) stood at

12.5 per cent, as compared to 10.1 per cent in the corresponding period a year ago (Figure 2).

The significant rise in reserve money has not translated into a commensurate increase in money

supply as the money multiplier has remained depressed due to a sharp rise in currency-deposit

ratio, and also large amount of funds parked under reverse repos with RBI.