Page 61 - ES 2020-21_Volume-1-2 [28-01-21]

P. 61

44 Economic Survey 2020-21 Volume 1

higher during economic crises than during economic booms – can ensure that the full

benefit of seminal economic reforms is reaped by limiting potential damage to productive

capacity. As the IRGD is expected to be negative in the foreseeable future, a fiscal policy

that provides an impetus to growth will lead to lower, not higher, debt-to-GDP ratios.

In fact, simulations undertaken till 2030 highlight that given India’s growth potential,

debt sustainability is unlikely to be a problem even in the worst scenarios. The chapter

thus demonstrates the desirability of using counter-cyclical fiscal policy to enable growth

during economic downturns.

While acknowledging the counterargument from critics that governments may have

a natural proclivity to spend, the Survey endeavours to provide the intellectual anchor

for the government to be more relaxed about debt and fiscal spending during a growth

slowdown or an economic crisis. The Survey’s call for more active, counter-cyclical fiscal

policy is not a call for fiscal irresponsibility. It is a call to break the intellectual anchoring

that has created an asymmetric bias against fiscal policy.

2.1 Amidst the Covid-19 crisis, fiscal policy has assumed enormous significance across the

world. Naturally, the debate around higher Government debt to support a fiscal expansion is

accompanied by concerns about its implications for future growth, debt sustainability, sovereign

ratings, and possible vulnerabilities on the external sector. This chapter examines the optimal

stance of fiscal policy in India during a crisis and establishes that the growth leads to debt

sustainability in the Indian context and not necessarily vice-versa.

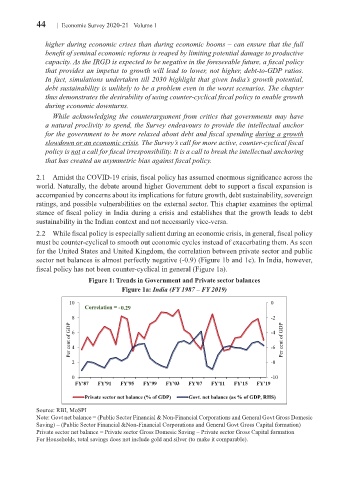

2.2 While fiscal policy is especially salient during an economic crisis, in general, fiscal policy

must be counter-cyclical to smooth out economic cycles instead of exacerbating them. As seen

for the United States and United Kingdom, the correlation between private sector and public

sector net balances is almost perfectly negative (-0.9) (Figure 1b and 1c). In India, however,

fiscal policy has not been counter-cyclical in general (Figure 1a).

Figure 1: Trends in Government and Private sector balances

Figure 1a: India (FY 1987 – FY 2019)

Source: RBI, MoSPI

Note: Govt net balance = (Public Sector Financial & Non-Financial Corporations and General Govt Gross Domesic

Saving) – (Public Sector Financial &Non-Financial Corporations and General Govt Gross Capital formation)

Private sector net balance = Private sector Gross Domesic Saving – Private sector Gross Capital formation

For Households, total savings does not include gold and silver (to make it comparable).