Page 134 - economic_survey_2021-2022

P. 134

108 Economic Survey 2021-22

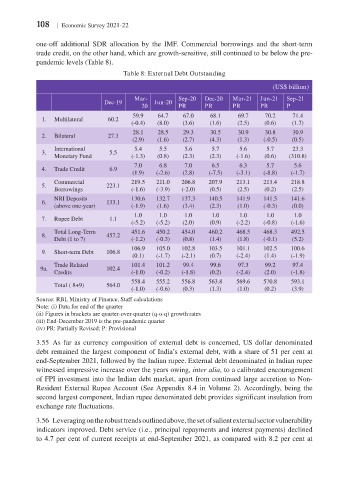

one-off additional SDR allocation by the IMF. Commercial borrowings and the short-term

trade credit, on the other hand, which are growth-sensitive, still continued to be below the pre-

pandemic levels (Table 8).

Table 8: External Debt Outstanding

(US$ billion)

Mar- Sep-20 Dec-20 Mar-21 Jun-21 Sep-21

Dec-19 Jun-20

20 PR PR PR PR P

59.9 64.7 67.0 68.1 69.7 70.2 71.4

1. Multilateral 60.2

(-0.4) (8.0) (3.6) (1.6) (2.5) (0.6) (1.7)

28.1 28.5 29.3 30.5 30.9 30.8 30.9

2. Bilateral 27.3

(2.9) (1.6) (2.7) (4.3) (1.3) (-0.5) (0.5)

International 5.4 5.5 5.6 5.7 5.6 5.7 23.3

3. 5.5

Monetary Fund (-1.3) (0.8) (2.3) (2.3) (-1.6) (0.6) (310.8)

7.0 6.8 7.0 6.5 6.3 5.7 5.6

4. Trade Credit 6.9

(1.9) (-2.6) (2.8) (-7.5) (-3.1) (-8.8) (-1.7)

Commercial 219.5 211.0 206.8 207.9 213.1 213.4 218.8

5. 223.1

Borrowings (-1.6) (-3.9) (-2.0) (0.5) (2.5) (0.2) (2.5)

NRI Deposits 130.6 132.7 137.3 140.5 141.9 141.5 141.6

6. 133.1

(above one-year) (-1.9) (1.6) (3.4) (2.3) (1.0) (-0.3) (0.0)

1.0 1.0 1.0 1.0 1.0 1.0 1.0

7. Rupee Debt 1.1

(-5.2) (-5.2) (2.0) (0.9) (-2.2) (-0.8) (-1.6)

Total Long-Term 451.6 450.2 454.0 460.2 468.5 468.3 492.5

8. 457.2

Debt (1 to 7) (-1.2) (-0.3) (0.8) (1.4) (1.8) (-0.1) (5.2)

106.9 105.0 102.8 103.5 101.1 102.5 100.6

9. Short-term Debt 106.8

(0.1) (-1.7) (-2.1) (0.7) (-2.4) (1.4) (-1.9)

Trade Related 101.4 101.2 99.4 99.6 97.3 99.2 97.4

9a. 102.4

Credits (-1.0) (-0.2) (-1.8) (0.2) (-2.4) (2.0) (-1.8)

558.4 555.2 556.8 563.8 569.6 570.8 593.1

Total ( 8+9) 564.0

(-1.0) (-0.6) (0.3) (1.3) (1.0) (0.2) (3.9)

Source: RBI, Ministry of Finance, Staff calculations

Note: (i) Data for end of the quarter

(ii) Figures in brackets are quarter-over-quarter (q-o-q) growth rates

(iii) End-December 2019 is the pre-pandemic quarter

(iv) PR: Partially Revised; P: Provisional

3.55 As far as currency composition of external debt is concerned, US dollar denominated

debt remained the largest component of India’s external debt, with a share of 51 per cent at

end-September 2021, followed by the Indian rupee. External debt denominated in Indian rupee

witnessed impressive increase over the years owing, inter alia, to a calibrated encouragement

of FPI investment into the Indian debt market, apart from continued large accretion to Non-

Resident External Rupee Account (See Appendix 8.4 in Volume 2). Accordingly, being the

second largest component, Indian rupee denominated debt provides significant insulation from

exchange rate fluctuations.

3.56 Leveraging on the robust trends outlined above, the set of salient external sector vulnerability

indicators improved. Debt service (i.e., principal repayments and interest payments) declined

to 4.7 per cent of current receipts at end-September 2021, as compared with 8.2 per cent at