Page 151 - economic_survey_2021-2022

P. 151

Monetary Management and Financial Intermediation 125

decision on 15 June 2021 to continue with the easy monetary policy stance kept the yields near

th

the 6 per cent mark.

4.15 In the beginning of second quarter (Q2) of 2021-22, yields started to rise. The announcement

of phased increase in the quantum of VRRR operations on 6 August 2021 and shift in market

th

sentiments to price in possibility of change in interest rate cycle sometime ahead also led to

some hardening of yields up to 6.26 per cent. The successively lower consumer price index

(CPI) prints, inclusion of the 10-year benchmark paper in the G-SAP auctions and no additional

borrowing by government for the second half of 2021-22 helped keep yields in check. The yield

on benchmark security stood at 6.22 per cent at the end of second quarter. In the third quarter

(Q3) of 2021-22, rise in US treasury yields and rising crude prices led the yields to inch higher

to 6.45 per cent at end-December 2021.

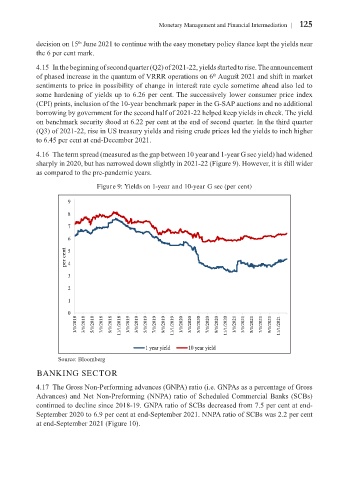

4.16 The term spread (measured as the gap between 10 year and 1-year G sec yield) had widened

sharply in 2020, but has narrowed down slightly in 2021-22 (Figure 9). However, it is still wider

as compared to the pre-pandemic years.

Figure 9: Yields on 1-year and 10-year G sec (per cent)

9

8

7

6

per cent 5 4

3

2

1

0

1/1/2018 3/1/2018 5/1/2018 7/1/2018 9/1/2018 11/1/2018 1/1/2019 3/1/2019 5/1/2019 7/1/2019 9/1/2019 11/1/2019 1/1/2020 3/1/2020 5/1/2020 7/1/2020 9/1/2020 11/1/2020 1/1/2021 3/1/2021 5/1/2021 7/1/2021 9/1/2021 11/1/2021

1 year yield 10 year yield

Source: Bloomberg

BANKING SECTOR

4.17 The Gross Non-Performing advances (GNPA) ratio (i.e. GNPAs as a percentage of Gross

Advances) and Net Non-Preforming (NNPA) ratio of Scheduled Commercial Banks (SCBs)

continued to decline since 2018-19. GNPA ratio of SCBs decreased from 7.5 per cent at end-

September 2020 to 6.9 per cent at end-September 2021. NNPA ratio of SCBs was 2.2 per cent

at end-September 2021 (Figure 10).