Page 146 - economic_survey_2021-2022

P. 146

120 Economic Survey 2021-22

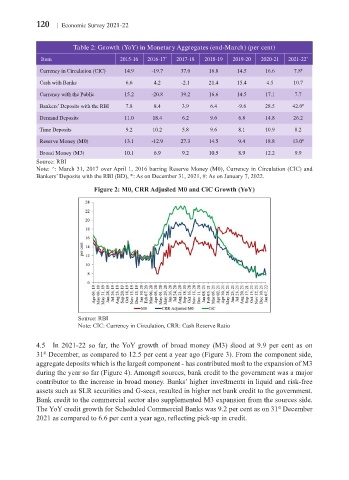

Table 2: Growth (YoY) in Monetary Aggregates (end-March) (per cent)

Item 2015-16 2016-17 ^ 2017-18 2018-19 2019-20 2020-21 2021-22 *

Currency in Circulation (CIC) 14.9 -19.7 37.0 16.8 14.5 16.6 7.8 #

Cash with Banks 6.6 4.2 -2.1 21.4 15.4 4.5 10.7

Currency with the Public 15.2 -20.8 39.2 16.6 14.5 17.1 7.7

Bankers’ Deposits with the RBI 7.8 8.4 3.9 6.4 -9.6 28.5 42.0 #

Demand Deposits 11.0 18.4 6.2 9.6 6.8 14.8 26.2

Time Deposits 9.2 10.2 5.8 9.6 8.1 10.9 8.2

Reserve Money (M0) 13.1 -12.9 27.3 14.5 9.4 18.8 13.0 #

Broad Money (M3) 10.1 6.9 9.2 10.5 8.9 12.2 9.9

Source: RBI

Note: ^: March 31, 2017 over April 1, 2016 barring Reserve Money (M0), Currency in Circulation (CIC) and

Bankers’ Deposits with the RBI (BD), *: As on December 31, 2021, #: As on January 7, 2022.

Figure 2: M0, CRR Adjusted M0 and CiC Growth (YoY)

Source: RBI

Note: CIC: Currency in Circulation, CRR: Cash Reserve Ratio

4.5 In 2021-22 so far, the YoY growth of broad money (M3) stood at 9.9 per cent as on

31 December, as compared to 12.5 per cent a year ago (Figure 3). From the component side,

st

aggregate deposits which is the largest component - has contributed most to the expansion of M3

during the year so far (Figure 4). Amongst sources, bank credit to the government was a major

contributor to the increase in broad money. Banks’ higher investments in liquid and risk-free

assets such as SLR securities and G-secs, resulted in higher net bank credit to the government.

Bank credit to the commercial sector also supplemented M3 expansion from the sources side.

The YoY credit growth for Scheduled Commercial Banks was 9.2 per cent as on 31 December

st

2021 as compared to 6.6 per cent a year ago, reflecting pick-up in credit.