Page 145 - economic_survey_2021-2022

P. 145

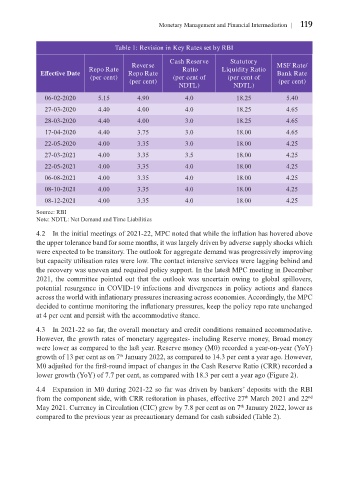

Monetary Management and Financial Intermediation 119

Table 1: Revision in Key Rates set by RBI

Cash Reserve Statutory

Reverse MSF Rate/

Repo Rate Ratio Liquidity Ratio

Effective Date Repo Rate Bank Rate

(per cent) (per cent of (per cent of

(per cent) (per cent)

NDTL) NDTL)

06-02-2020 5.15 4.90 4.0 18.25 5.40

27-03-2020 4.40 4.00 4.0 18.25 4.65

28-03-2020 4.40 4.00 3.0 18.25 4.65

17-04-2020 4.40 3.75 3.0 18.00 4.65

22-05-2020 4.00 3.35 3.0 18.00 4.25

27-03-2021 4.00 3.35 3.5 18.00 4.25

22-05-2021 4.00 3.35 4.0 18.00 4.25

06-08-2021 4.00 3.35 4.0 18.00 4.25

08-10-2021 4.00 3.35 4.0 18.00 4.25

08-12-2021 4.00 3.35 4.0 18.00 4.25

Source: RBI

Note: NDTL: Net Demand and Time Liabilities

4.2 In the initial meetings of 2021-22, MPC noted that while the inflation has hovered above

the upper tolerance band for some months, it was largely driven by adverse supply shocks which

were expected to be transitory. The outlook for aggregate demand was progressively improving

but capacity utilisation rates were low. The contact intensive services were lagging behind and

the recovery was uneven and required policy support. In the latest MPC meeting in December

2021, the committee pointed out that the outlook was uncertain owing to global spillovers,

potential resurgence in COVID-19 infections and divergences in policy actions and stances

across the world with inflationary pressures increasing across economies. Accordingly, the MPC

decided to continue monitoring the inflationary pressures, keep the policy repo rate unchanged

at 4 per cent and persist with the accommodative stance.

4.3 In 2021-22 so far, the overall monetary and credit conditions remained accommodative.

However, the growth rates of monetary aggregates- including Reserve money, Broad money

were lower as compared to the last year. Reserve money (M0) recorded a year-on-year (YoY)

growth of 13 per cent as on 7 January 2022, as compared to 14.3 per cent a year ago. However,

th

M0 adjusted for the first-round impact of changes in the Cash Reserve Ratio (CRR) recorded a

lower growth (YoY) of 7.7 per cent, as compared with 18.3 per cent a year ago (Figure 2).

4.4 Expansion in M0 during 2021-22 so far was driven by bankers’ deposits with the RBI

from the component side, with CRR restoration in phases, effective 27 March 2021 and 22 nd

th

May 2021. Currency in Circulation (CIC) grew by 7.8 per cent as on 7 January 2022, lower as

th

compared to the previous year as precautionary demand for cash subsided (Table 2).