Page 230 - ES 2020-21_Volume-1-2 [28-01-21]

P. 230

Regulatory Forbearance: An Emergency Medicine, Not Staple Diet! 213

interest expense. Firms with an interest coverage ratio lower than one are unable to meet their

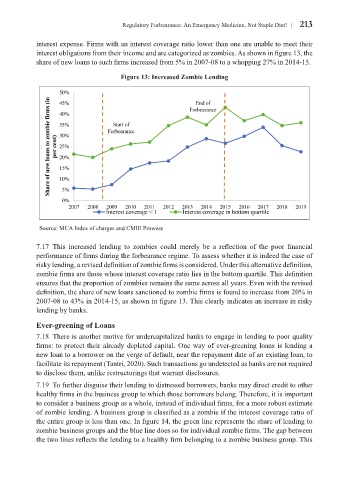

interest obligations from their income and are categorized as zombies. As shown in figure 13, the

share of new loans to such firms increased from 5% in 2007-08 to a whopping 27% in 2014-15.

Figure 13: Increased Zombie Lending

Source: MCA Index of charges and CMIE Prowess

7.17 This increased lending to zombies could merely be a reflection of the poor financial

performance of firms during the forbearance regime. To assess whether it is indeed the case of

risky lending, a revised definition of zombie firms is considered. Under this alternative definition,

zombie firms are those whose interest coverage ratio lies in the bottom quartile. This definition

ensures that the proportion of zombies remains the same across all years. Even with the revised

definition, the share of new loans sanctioned to zombie firms is found to increase from 20% in

2007-08 to 43% in 2014-15, as shown in figure 13. This clearly indicates an increase in risky

lending by banks.

Ever-greening of Loans

7.18 There is another motive for undercapitalized banks to engage in lending to poor quality

firms: to protect their already depleted capital. One way of ever-greening loans is lending a

new loan to a borrower on the verge of default, near the repayment date of an existing loan, to

facilitate its repayment (Tantri, 2020). Such transactions go undetected as banks are not required

to disclose them, unlike restructurings that warrant disclosures.

7.19 To further disguise their lending to distressed borrowers, banks may direct credit to other

healthy firms in the business group to which those borrowers belong. Therefore, it is important

to consider a business group as a whole, instead of individual firms, for a more robust estimate

of zombie lending. A business group is classified as a zombie if the interest coverage ratio of

the entire group is less than one. In figure 14, the green line represents the share of lending to

zombie business groups and the blue line does so for individual zombie firms. The gap between

the two lines reflects the lending to a healthy firm belonging to a zombie business group. This