Page 235 - ES 2020-21_Volume-1-2 [28-01-21]

P. 235

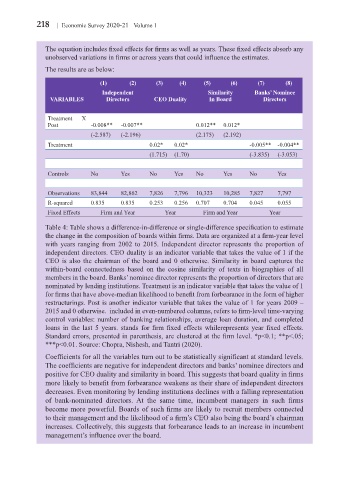

218 Economic Survey 2020-21 Volume 1

The equation includes fixed effects for firms as well as years. These fixed effects absorb any

unobserved variations in firms or across years that could influence the estimates.

The results are as below:

(1) (2) (3) (4) (5) (6) (7) (8)

Independent Similarity Banks’ Nominee

VARIABLES Directors CEO Duality In Board Directors

Treatment X

Post -0.008** -0.007** 0.012** 0.012*

(-2.587) (-2.196) (2.175) (2.192)

Treatment 0.02* 0.02* -0.005** -0.004**

(1.715) (1.70) (-3.835) (-3.053)

Controls No Yes No Yes No Yes No Yes

Observations 83,844 82,862 7,826 7,796 10,323 10,285 7,827 7,797

R-squared 0.835 0.835 0.253 0.256 0.707 0.704 0.045 0.055

Fixed Effects Firm and Year Year Firm and Year Year

Table 4: Table shows a difference-in-difference or single-difference specification to estimate

the change in the composition of boards within firms. Data are organized at a firm-year level

with years ranging from 2002 to 2015. Independent director represents the proportion of

independent directors. CEO duality is an indicator variable that takes the value of 1 if the

CEO is also the chairman of the board and 0 otherwise. Similarity in board captures the

within-board connectedness based on the cosine similarity of texts in biographies of all

members in the board. Banks’ nominee director represents the proportion of directors that are

nominated by lending institutions. Treatment is an indicator variable that takes the value of 1

for firms that have above-median likelihood to benefit from forbearance in the form of higher

restructurings. Post is another indicator variable that takes the value of 1 for years 2009 –

2015 and 0 otherwise. included in even-numbered columns, refers to firm-level time-varying

control variables: number of banking relationships, average loan duration, and completed

loans in the last 5 years. stands for firm fixed effects whilerepresents year fixed effects.

Standard errors, presented in parenthesis, are clustered at the firm level. *p<0.1; **p<.05;

***p<0.01. Source: Chopra, Nishesh, and Tantri (2020).

Coefficients for all the variables turn out to be statistically significant at standard levels.

The coefficients are negative for independent directors and banks’ nominee directors and

positive for CEO duality and similarity in board. This suggests that board quality in firms

more likely to benefit from forbearance weakens as their share of independent directors

decreases. Even monitoring by lending institutions declines with a falling representation

of bank-nominated directors. At the same time, incumbent managers in such firms

become more powerful. Boards of such firms are likely to recruit members connected

to their management and the likelihood of a firm’s CEO also being the board’s chairman

increases. Collectively, this suggests that forbearance leads to an increase in incumbent

management’s influence over the board.