Page 483 - ES 2020-21_Volume-1-2 [28-01-21]

P. 483

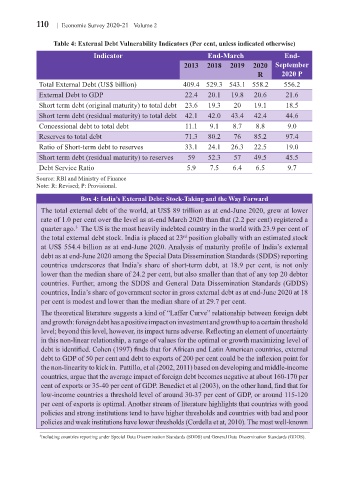

110 Economic Survey 2020-21 Volume 2

Table 4: External Debt Vulnerability Indicators (Per cent, unless indicated otherwise)

Indicator End-March End-

2013 2018 2019 2020 September

R 2020 P

Total External Debt (US$ billion) 409.4 529.3 543.1 558.2 556.2

External Debt to GDP 22.4 20.1 19.8 20.6 21.6

Short term debt (original maturity) to total debt 23.6 19.3 20 19.1 18.5

Short term debt (residual maturity) to total debt 42.1 42.0 43.4 42.4 44.6

Concessional debt to total debt 11.1 9.1 8.7 8.8 9.0

Reserves to total debt 71.3 80.2 76 85.2 97.4

Ratio of Short-term debt to reserves 33.1 24.1 26.3 22.5 19.0

Short term debt (residual maturity) to reserves 59 52.3 57 49.5 45.5

Debt Service Ratio 5.9 7.5 6.4 6.5 9.7

Source: RBI and Ministry of Finance

Note: R: Revised; P: Provisional.

Box 4: India’s External Debt: Stock-Taking and the Way Forward

The total external debt of the world, at US$ 89 trillion as at end-June 2020, grew at lower

rate of 1.0 per cent over the level as at-end March 2020 than that (2.2 per cent) registered a

quarter ago. The US is the most heavily indebted country in the world with 23.9 per cent of

3

the total external debt stock. India is placed at 23 position globally with an estimated stock

rd

at US$ 554.4 billion as at end-June 2020. Analysis of maturity profile of India’s external

debt as at end-June 2020 among the Special Data Dissemination Standards (SDDS) reporting

countries underscores that India’s share of short-term debt, at 18.9 per cent, is not only

lower than the median share of 24.2 per cent, but also smaller than that of any top 20 debtor

countries. Further, among the SDDS and General Data Dissemination Standards (GDDS)

countries, India’s share of government sector in gross external debt as at end-June 2020 at 18

per cent is modest and lower than the median share of at 29.7 per cent.

The theoretical literature suggests a kind of “Laffer Curve” relationship between foreign debt

and growth: foreign debt has a positive impact on investment and growth up to a certain threshold

level; beyond this level, however, its impact turns adverse. Reflecting an element of uncertainty

in this non-linear relationship, a range of values for the optimal or growth maximizing level of

debt is identified. Cohen (1997) finds that for African and Latin American countries, external

debt to GDP of 50 per cent and debt to exports of 200 per cent could be the inflexion point for

the non-linearity to kick in. Pattillo, et al (2002, 2011) based on developing and middle-income

countries, argue that the average impact of foreign debt becomes negative at about 160-170 per

cent of exports or 35-40 per cent of GDP. Benedict et al (2003), on the other hand, find that for

low-income countries a threshold level of around 30-37 per cent of GDP, or around 115-120

per cent of exports is optimal. Another stream of literature highlights that countries with good

policies and strong institutions tend to have higher thresholds and countries with bad and poor

policies and weak institutions have lower thresholds (Cordella et at, 2010). The most well-known

3 Including countries reporting under Special Data Dissemination Standards (SDDS) and General Data Dissemination Standards (GDDS).