Page 487 - ES 2020-21_Volume-1-2 [28-01-21]

P. 487

114 Economic Survey 2020-21 Volume 2

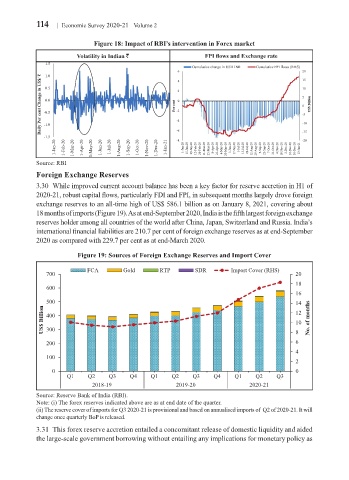

Figure 18: Impact of RBI’s intervention in Forex market

Volatility in Indian ` FPI flows and Exchange rate

1.5

Cumulative change in USD INR Cumulative FPI flows (RHS)

6 4 20

1.0

Daily Per cent Change in US$/ ₹ -0.5 Per cent -2 -4 2 0 10 US$ Billion

15

0.5

5

0.0

0

-5

-1.0

-15

-1.5 -6 -8 -10

-20

1-Jan-20 1-Feb-20 1-Mar-20 1-Apr-20 1-May-20 1-Jun-20 1-Jul-20 1-Aug-20 1-Sep-20 1-Oct-20 1-Nov-20 1-Dec-20 1-Jan-21 1-Jan-20 15-Jan-20 29-Jan-20 12-Feb-20 26-Feb-20 11-Mar-20 25-Mar-20 8-Apr-20 22-Apr-20 6-May-20 20-May-20 3-Jun-20 17-Jun-20 1-Jul-20 15-Jul-20 29-Jul-20 12-Aug-20 26-Aug-20 9-Sep-20 23-Sep-20 7-Oct-20 21-Oct-20 4-Nov-20 18-Nov-20 2-Dec-20 16-Dec-20 30-Dec-20 13-Jan-21

Source: RBI

Foreign Exchange Reserves

3.30 While improved current account balance has been a key factor for reserve accretion in H1 of

2020-21, robust capital flows, particularly FDI and FPI, in subsequent months largely drove foreign

exchange reserves to an all-time high of US$ 586.1 billion as on January 8, 2021, covering about

18 months of imports (Figure 19). As at end-September 2020, India is the fifth largest foreign exchange

reserves holder among all countries of the world after China, Japan, Switzerland and Russia. India’s

international financial liabilities are 210.7 per cent of foreign exchange reserves as at end-September

2020 as compared with 229.7 per cent as at end-March 2020.

Figure 19: Sources of Foreign Exchange Reserves and Import Cover

FCA Gold RTP SDR Import Cover (RHS)

700 20

18

600

16

500 14

US$ Billion 400 12 No. of months

10

300

8

200 6

4

100

2

0 0

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2018-19 2019-20 2020-21

Source: Reserve Bank of India (RBI).

Note: (i) The forex reserves indicated above are as at end date of the quarter.

(ii) The reserve cover of imports for Q3 2020-21 is provisional and based on annualised imports of Q2 of 2020-21. It will

change once quarterly BoP is released.

3.31 This forex reserve accretion entailed a concomitant release of domestic liquidity and aided

the large-scale government borrowing without entailing any implications for monetary policy as